Quick Summary

This article explains 8 hidden dangers of irrevocable trusts, including loss of control, tax complications, and liquidity challenges. Knowing these risks is essential before committing. Learn how to protect your assets through smart trust design and legal safeguards. For more insight into trust planning and offshore strategies, explore our other articles on asset protection.

Looking to Set Up an Irrevocable Trust? Know the Risks First

Irrevocable trusts are powerful tools, but they come with risks that many do not see until it is too late. At Blake Harris Law, we help clients understand these risks before making permanent decisions.

This Blake Harris Law article outlines the 8 most common dangers you may encounter with irrevocable trusts.

Why Listen to Us?

At Blake Harris Law, we offer proven asset protection strategies, including Cook Islands, Nevis, and Belize Trusts, to safeguard assets from lawsuits and divorce. Our clients commend our firm’s reliability and personalized service.

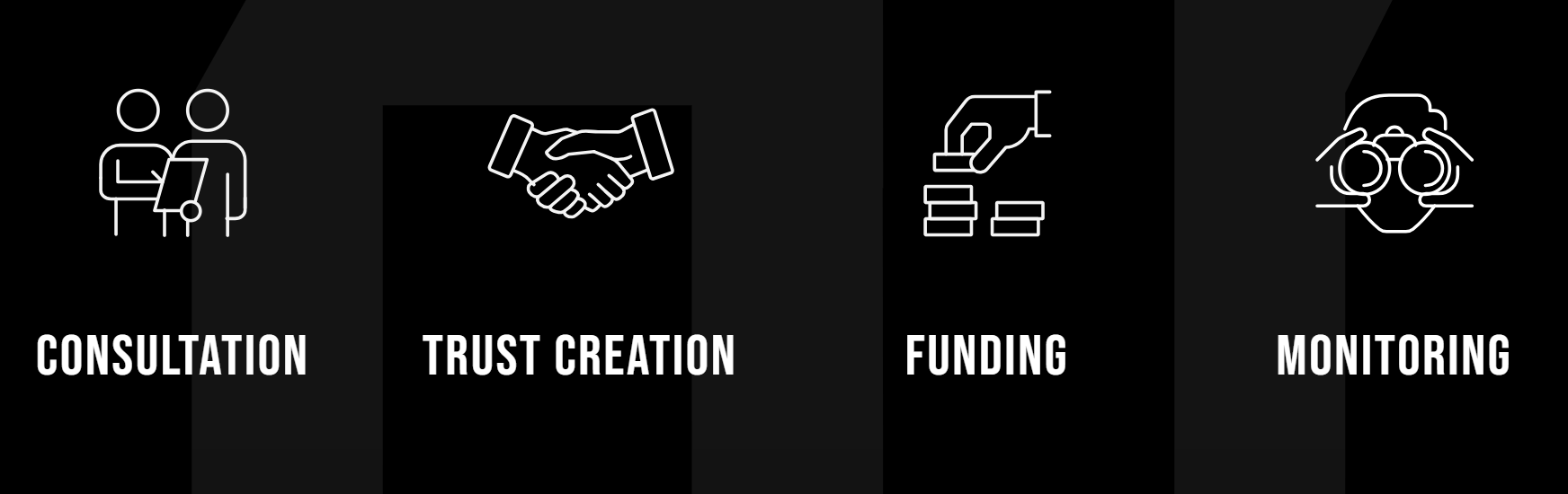

Our four-step process ensures tailored, confidential solutions for high-net-worth individuals.

What Is an Irrevocable Trust?

An irrevocable trust is a legal structure that transfers ownership of assets such as cryptocurrency, real estate, or business interests, out of your name permanently. Once formed, the terms cannot be changed without court involvement or beneficiary consent.

This structure helps limit legal exposure and protects assets from potential claims. It also removes assets from your taxable estate, which may reduce estate taxes.

The tradeoff is control. You cannot access or direct the assets like before. That is why we design trusts carefully at Blake Harris Law, often using Cook Islands, Nevis, or Belize jurisdictions for added privacy and protection.

Why Is It Important to Understand Irrevocable Trusts?

- Loss of Control: Once assets are in an irrevocable trust, you no longer own or manage them. This can affect how you access or use those assets.

- Tax Impact: Trusts can shift estate and income tax burdens. Without planning, you may trigger unintended tax consequences.

- Legal Protection: A well-structured trust can shield assets from potential claims. A poorly drafted one may not hold up under scrutiny.

- Inflexibility: Modifying terms later is difficult. Understanding limitations upfront avoids future regrets.

8 Hidden Dangers of an Irrevocable Trust

- Loss of Control Over Assets

- Inflexibility in Modifying Trust Terms

- Potential Tax Implications

- Risk of Trustee Mismanagement

- Impact on Medicaid Eligibility

- Complexity and Associated Costs

- Possible Loss of Principal Amount Invested

- Challenges with Asset Liquidity

1. Loss of Control Over Assets

An irrevocable trust removes legal ownership of your assets. Once transferred, you no longer hold title to them, your trustee does. That is the core tradeoff.

This loss of control is not just legal. It affects how you can interact with the assets day to day. You cannot:

- Withdraw funds or reassign distributions without trustee approval

- Modify how real estate, cryptocurrency, or business interests are managed

- Reverse decisions once the trust is funded

For high-net-worth individuals, this creates real tension. The more wealth you move into the trust, the more reliant you become on the trustee’s actions and judgment.

At Blake Harris Law, we address this risk through careful structural design. We work with independent, licensed trustees in the Cook Islands, Nevis, and Belize, jurisdictions with strong legal protections and predictable enforcement. This helps ensure the trustee operates in line with the trust’s purpose and your original intent.

We also build in layers of oversight and flexibility where permitted, including:

- Trust protectors, who hold powers to replace trustees if needed

- Limited powers of appointment, which let you influence future distributions

- Entities like Nevis LLCs, owned by the trust but controlled by trusted managers

These tools do not restore full control, but they do help align the trust’s operation with your goals.

Understanding this shift in control, what you give up, and what safeguards you can build in, is essential to making the right trust decision.

2. Inflexibility in Modifying Trust Terms

Irrevocable trusts are designed to be permanent. Once signed and funded, you cannot revoke or easily amend them. That is the strategic risk.

Most clients assume some flexibility remains. In practice, change requires unanimous beneficiary consent or court involvement. This creates friction when:

- Tax laws shift and expose you to new liabilities

- A trustee underperforms or becomes uncooperative

- Family or business dynamics evolve in ways the trust never anticipated

These scenarios are common. Without the right mechanisms in place, your options will be limited or expensive.

At Blake Harris Law, we address this in the trust creation phase. We structure trusts to include key tools that preserve lawful flexibility:

- Trust Protectors: Appointed third parties who can replace trustees or approve limited changes

- Powers of Appointment: Built-in rights to shift asset distributions or add beneficiaries

- Jurisdictional Leverage: We use jurisdictions like the Cook Islands, Nevis, and Belize that offer robust statutes for modification and enforcement

Each of these features creates pathways to respond to change while preserving asset protection. You still give up direct control, but you do not give up options.

If your financial future spans decades, your trust design should, too. That means planning not just for today, but for what might come next.

3. Potential Tax Implications

Irrevocable trusts trigger unique tax rules. These rules can reduce estate taxes, but also create traps if not planned correctly. For high-net-worth individuals, the cost of a misstep can be steep.

Trusts are separate tax entities. That means:

- The trust must file its own return (Form 1041)

- Income retained in the trust is taxed at compressed rates—reaching 37% at just $15,200 (2024 threshold)

- Deductions and credits are limited compared to individual returns

Improper drafting can also eliminate key tax advantages. If a primary residence is transferred without careful structuring, you may lose the capital gains exclusion on a future sale. Income-generating assets may also lose step-up basis protections, increasing future tax exposure.

Our firm structures trusts to avoid these pitfalls. We collaborate with CPAs to align trust design with your broader tax plan. When appropriate, we use grantor trust status to retain favorable income tax treatment while preserving asset protection.

Jurisdiction matters here, too. Trusts formed in the Cook Islands, Nevis, or Belize can offer more flexibility in managing foreign income reporting and trust classification under IRS rules, if structured properly.

Tax exposure is not just about rates. It is about structure, jurisdiction, and proactive planning. We treat it that way.

4. Risk of Trustee Mismanagement

Irrevocable trusts shift legal control to the trustee. That makes trustee selection the single most important operational decision you will make.

Trustees control distributions, manage investments, and handle tax filings. If a trustee acts carelessly or with bias, it can damage the trust’s performance, or even trigger legal challenges. This risk compounds when trusts hold high-volatility assets like cryptocurrency or illiquid holdings such as private equity or real estate.

Mismanagement can include:

- Failing to diversify investments or follow prudent investor rules

- Overpaying themselves or outside advisors

- Ignoring beneficiary needs or breaching fiduciary duties

Our team solves for this by working only with licensed trustees in asset protection jurisdictions like the Cook Islands, Nevis, and Belize. For instance, attorney Sheila Arnado brings international legal experience and cross-border insight that supports our offshore trust strategies. These jurisdictions enforce strict fiduciary standards, making it easier to hold trustees accountable.

We also recommend appointing a trust protector. This role provides oversight and authority to remove and replace a trustee without court action. It is one of the most effective ways to keep the structure aligned with your goals.

5. Impact on Medicaid Eligibility

Irrevocable trusts are often used in Medicaid planning, but poor timing or structure can backfire. The government applies a five-year “look-back” period when evaluating asset transfers. If assets are moved into a trust within that window, they may still count against you.

This issue is especially common with:

- Residential property transferred too close to the application date

- Trusts that grant the applicant indirect benefits or access

- Improperly drafted distribution clauses that violate Medicaid rules

The result? Disqualification, penalties, or delayed eligibility, just when long-term care becomes urgent.

If long-term care planning is a priority, it must be built into the trust’s legal and operational design from the start. That includes:

- Avoiding retained interest that triggers inclusion in eligibility formulas

- Timing the transfer well in advance of care needs

- Ensuring compliance with both federal and state rules

Medicaid planning and asset protection are not always compatible. When they are, it takes precision, not assumptions.

6. Complexity and Associated Costs

Irrevocable trusts are not plug-and-play. They require tailored planning, multi-jurisdictional coordination, and ongoing administration. That complexity comes at a price, and the costs add up fast.

Expect to pay for:

- Legal structuring and review

- Trustee fees, especially with offshore jurisdictions like the Cook Islands, Nevis, or Belize

- Annual tax filings, accounting support, and possible valuation reports

- Ongoing communication between advisors, including legal, tax, and financial teams

Many high-net-worth individuals underestimate the administrative layer. Managing a trust that holds cryptocurrency, foreign accounts, or private business interests requires precision and regulatory awareness. A mistake in reporting or recordkeeping can trigger IRS scrutiny or compromise the trust’s asset protection.

We streamline this process with a four-step system: consultation, trust creation, funding, and ongoing support. We collaborate with accountants and fiduciaries to ensure the structure is legally sound and functionally efficient.

Like any structure, an irrevocable trust needs maintenance, coordination, and smart oversight to deliver the protection it promises. Without that, the costs, both financial and legal, can outweigh the benefits.

7. Possible Loss of Principal Amount Invested

An irrevocable trust protects legal ownership, but not investment performance. Once you fund the trust, you also give up investment authority unless you structure otherwise.

If the trustee chooses poor allocations, or market volatility impacts performance (especially in crypto or private assets), the trust may lose value. Unlike a personal brokerage account, you cannot simply move the funds or change direction.

Common risk points include:

- Overconcentration in a single asset class

- Failure to hedge or rebalance

- Illiquid investments held without proper exit planning

At Blake Harris Law, we reduce this risk during the setup phase. For clients funding trusts with complex or volatile holdings such as cryptocurrency, real estate, or business equity, we recommend using a controlled LLC owned by the trust. This structure separates day-to-day asset management from legal ownership.

This gives clients the ability to:

- Appoint a trusted manager to oversee investments

- Maintain control over how assets are deployed within the protective shell

- Create a clear division between management and legal ownership for liability purposes

Protection does not mean performance. Asset growth requires strategy, especially when control shifts to someone else. A well-structured trust anticipates risk and installs the tools needed to manage it legally and effectively.

8. Challenges with Asset Liquidity

Irrevocable trusts protect assets, but they can complicate how and when you access cash. Liquidity becomes a strategic concern, especially when the trust holds illiquid assets like real estate, closely held businesses, or cryptocurrency.

The challenge is structural. Trusts do not function like checking accounts. Distributions require trustee approval, and trustees are bound by fiduciary duties, not convenience. If liquidity planning is overlooked, you may find:

- Delays in meeting tax obligations or personal cash needs

- Forced sales of trust assets at inopportune times

- Inability to capitalize on time-sensitive investments or emergencies

For trusts funded with less liquid holdings, asset-segregation strategies may help, which include:

- Funding a parallel sub-trust or LLC with liquid reserves

- Building in scheduled distribution triggers based on milestones or needs

- Designating flexible investment policies for the trustee

For example, a trust may hold a Nevis LLC that owns real estate and digital assets, while a separate Belize account holds liquid reserves. This split approach balances long-term growth with short-term responsiveness.

Protection without liquidity creates risk, not just inconvenience. A solid trust structure ensures that while your assets are secure, they remain strategically available when life, business, or markets shift.

Trust Blake Harris Law to Guide You

Irrevocable trusts offer strong asset protection, but they come with real risks: loss of control, limited flexibility, tax exposure, liquidity issues, and more. Understanding these tradeoffs is key. That is where Blake Harris Law comes in.

We build and manage irrevocable trusts designed for high-net-worth individuals, using proven strategies across the Cook Islands, Nevis, and Belize. Our focus: protect assets, preserve flexibility, and plan with clarity.

Secure your legacy with confidence—contact Blake Harris Law to build smarter trust structures.