What Is a Cook Islands Trust?

A Cook Islands Trust is an irrevocable offshore trust established under the laws of the Cook Islands, a self-governing nation in free association with New Zealand. It is governed by the International Trusts Act, first enacted in 1984 and strengthened through amendments — most significantly in 1989.

At its core, a trust is a legal arrangement in which a settlor transfers legal ownership of assets to a trustee, who manages them for designated beneficiaries. What makes a Cook Islands Trust different from every domestic alternative is not its basic structure but the legal environment governing it: a system that does not recognize U.S. court judgments, imposes the criminal-law evidentiary standard on creditors, and requires any legal attack to start from scratch under Cook Islands law.

Cook Islands trusts are not about secrecy. They are about jurisdictional strength.

Why the Cook Islands?

The Cook Islands did not become the world's most-trusted asset-protection jurisdiction by accident. In the early 1980s, policymakers chose a single objective: build the strongest statutory protection framework available, and defend it.

The result is a track record no other jurisdiction can match. Cook Islands trusts have been challenged by determined, well-funded creditors — including the Federal Trade Commission — in real adversarial litigation, and the structure has held. The jurisdiction's courts have applied its laws as intended. Its legislature has updated its statutes to respond to evolving legal challenges while preserving the core protections. Its regulatory framework meets international standards for anti-money laundering and transparency, which means the Cook Islands retains access to global banking that more opaque jurisdictions lose.

The New Zealand Relationship

The Cook Islands is a self-governing nation in free association with New Zealand, a status established in 1965 that grants the Cook Islands full authority over its legal system, financial regulations, and trust laws. New Zealand does not govern the Cook Islands. A New Zealand judgment is no more automatically enforceable in the Cook Islands than a U.S. one.

What the relationship does provide is credibility. New Zealand is widely regarded for strong institutions and rule of law. The constitutional link signals that the Cook Islands operates within a recognized international framework — even as it preserves the legislative independence that makes its asset-protection laws effective. That credibility helps it maintain banking relationships that more isolated offshore centers lose.

Political and Legal Stability

For asset protection, predictability matters as much as strength. The Cook Islands has maintained a consistent approach to its financial services industry for decades. The legal framework has remained stable. The jurisdiction has resisted external pressure to weaken its asset-protection statutes while adapting to international compliance requirements. Strong laws, consistent enforcement, international credibility, and decades of tested performance — this is why experienced asset-protection attorneys direct clients facing serious exposure to the Cook Islands.

How a Trust Works

A trust is a legal arrangement, not a company or a separate legal person. One party (the settlor) transfers legal ownership of assets to another (the trustee), who manages them for designated beneficiaries. The settlor no longer legally owns the assets, so creditors cannot reach them as if they were the settlor's property.

That division between legal ownership and beneficial enjoyment is the foundational principle of trust law. In an asset-protection context, it is also the mechanism that creates the protection.

For the complete step-by-step mechanics, see How a Cook Islands Trust Works.

The International Trusts Act

The Cook Islands International Trusts Act is the legal foundation that separates a Cook Islands Trust from every other asset-protection structure. First enacted in 1984 and strengthened by landmark amendments in 1989, it was not adapted from existing trust law — it was purpose-built to resist foreign creditor claims. Five features do the work:

- No foreign-judgment enforcement. U.S. judgments are not recognized. A creditor must start a new case in Cook Islands courts from scratch.

- Beyond-a-reasonable-doubt evidentiary standard. The criminal-law burden of proof, applied to civil fraudulent-transfer claims. No other asset-protection jurisdiction imposes a higher burden on creditors.

- Short statute of limitations. Generally one to two years from the date of transfer. Once the window closes, Cook Islands courts will not hear the claim.

- The duress clause. When a U.S. court orders repatriation, the duress clause activates and the trustee — bound by Cook Islands law, not U.S. orders — is required to refuse. See Duress Clauses Explained.

- Licensed-trustee oversight. Trustees must be licensed by the Cook Islands Financial Services Authority, which enforces professional and operational standards.

For a deeper plain-English walk-through of the statute, see The Cook Islands International Trusts Act 1984.

The Four Key Parties

A Cook Islands Trust is defined by a formal legal document — the trust deed — and operates through four clearly defined roles.

Fig. 1 — Trust Structure

Settlor

The asset owner. Transfers assets into the trust.

Cook Islands Trust

Governed by deed under the International Trusts Act. Holds and protects the assets.

Trustee

Holds legal title to assets. Licensed in the Cook Islands, regulated by the FSA.

Protector

Oversees the trustee. Independent. May veto decisions and replace the trustee when warranted.

Beneficiaries

The settlor and the settlor's family.

- The settlor creates the trust and transfers assets into it. After transfer the settlor no longer holds legal title and cannot demand distributions. This relinquishment of control is the design feature that makes the structure work.

- The trustee holds legal title and manages the assets under fiduciary obligation and Cook Islands law. The trustee must be licensed in the Cook Islands and must exercise genuine independent discretion — not reflexive compliance with the settlor's wishes.

- The protector is an optional but common role that provides oversight of the trustee, with limited powers to veto specific decisions or replace the trustee. The protector must be genuinely independent to serve their intended purpose.

- The beneficiaries are typically the settlor and family, holding discretionary rather than fixed interests. If a beneficiary cannot compel a distribution, neither can their creditor.

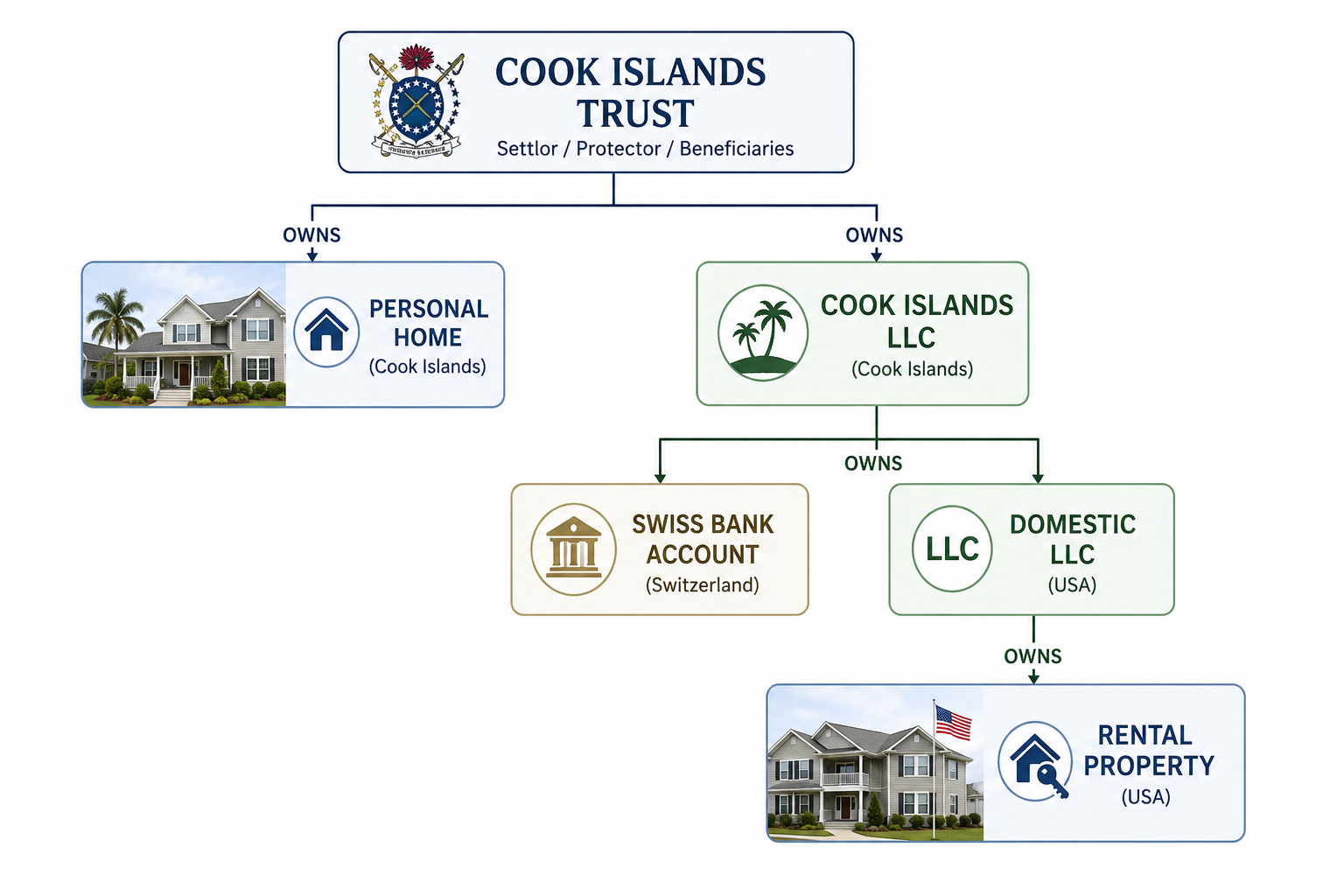

Most structures pair the trust with a Cook Islands LLC: the trust owns the LLC, and the settlor manages the LLC's day-to-day operations until a legal threat activates the duress clause. For the full breakdown, see Trustee, Protector, and Settlor and Cook Islands Trust vs. Offshore LLC.

Who Needs a Cook Islands Trust?

Asset-protection planning is not reserved for the ultra-wealthy. The modern U.S. legal climate has expanded the universe of individuals facing real, meaningful exposure — and those who wait until a claim appears have already waited too long.

- Medical professionals. Malpractice insurance is a critical first layer, but coverage limits get exceeded and some liabilities fall outside policy coverage entirely. A Cook Islands Trust creates the backstop. See Cook Islands Trust for Physicians.

- Business owners. Personal guarantees, piercing the corporate veil, and operational missteps can extend liability past the business entity. See Cook Islands Trust for Business Owners.

- High-net-worth individuals and families. Wealth creates a target. The perception of resources alone shapes how aggressively claims get pursued. See Cook Islands Trust for High-Net-Worth Families.

- Real estate investors. Property ownership generates ongoing exposure to tenant disputes, premises liability, and contractual conflicts across every asset in a portfolio. See Cook Islands Trust for Real Estate Investors.

- Cryptocurrency holders. Concentrated digital-asset wealth is just as vulnerable to civil judgments as a brokerage account — and presents specific custody and reporting questions. See Cook Islands Trust for Cryptocurrency.

01 — Exposure Tool

How exposed are you?

Calculated exposure

HIGH

out of 100

Your profile and asset level put you in the top tier of likely lawsuit targets.

At this risk level the question is timing and execution, not whether to plan. A free consultation will show you what a structure looks like for your specifics.

Book consultation →Heuristic only — not legal advice

A Cook Islands Trust is not appropriate for individuals currently facing active criminal charges or government enforcement actions, those attempting to shield assets from an ongoing legal proceeding, or those whose asset base does not justify the cost. If any of those apply, we will tell you directly and recommend an alternative.

Cook Islands Trust vs. Domestic Asset Protection Trust

Domestic asset-protection trusts (DAPTs) set up in Nevada, Delaware, Alaska, or other DAPT-friendly states are often marketed as a simpler, cheaper alternative to offshore planning. They are not equivalent. The difference is not a matter of degree — it is a matter of jurisdiction. A domestic trust exists within the same legal system a U.S. creditor will use to pursue you. U.S. courts can issue orders directly to a domestic trustee, freeze accounts, and override state-level protections under federal bankruptcy law.

Cook Islands Trust vs. Domestic Asset Protection Trust — at a glance

| Dimension | Cook Islands Trust | Domestic APT (Nevada, Delaware, Alaska, etc.) |

|---|---|---|

| Governing jurisdiction | Cook Islands law; outside the reach of U.S. courts | U.S. state law; fully within the reach of U.S. courts |

| Statute of limitations on fraudulent-transfer claims | 1–2 years from the date of transfer | Up to 10 years under federal bankruptcy law (11 U.S.C. § 548(e)) |

| Evidentiary standard for creditors | Beyond a reasonable doubt | Preponderance of the evidence (some states clear and convincing) |

| Foreign judgment enforcement | Cook Islands courts do not recognize U.S. judgments | Full Faith and Credit applies — any state's judgment is enforceable |

| Federal bankruptcy override | None — trust property sits outside U.S. court reach | Trust assets remain reachable in U.S. bankruptcy proceedings |

| Trustee subject to U.S. court orders | No — licensed Cook Islands fiduciary | Yes — domestic trustee is fully within U.S. jurisdiction |

| Track record under contested litigation | 40+ years of adverse case law; structure has held | Mixed; multiple structural defeats (e.g. In re Huber, In re Mortensen) |

| Engagement cost at Blake Harris Law | $25,000 setup · $7,000/year | Varies; typically lower upfront with greater downstream exposure |

The same jurisdictional problem applies to Hybrid DAPTs and the Bridge Trust® model. Both remain fully within U.S. court reach until a creditor event triggers an attempted offshore transition — at the worst possible moment, when fraudulent-transfer scrutiny is most intense. For the full comparison, see Cook Islands Trust vs. Domestic Asset Protection Trust, The Hybrid DAPT, and The Bridge Trust® Analysis.

Cook Islands vs. Other Offshore Jurisdictions

The Cook Islands is not the only offshore jurisdiction offering asset-protection trusts. Nevis, Belize, and the Cayman Islands are frequently discussed as alternatives. Each has genuine strengths, but they are not equivalent — and the differences matter when assets are actually under threat.

Offshore trust jurisdictions compared

| Dimension | Cook Islands | Nevis | Belize | Cayman Islands |

|---|---|---|---|---|

| Evidentiary standard for creditors | Beyond a reasonable doubt | Clear and convincing | Clear and convincing | Civil standard (varies by claim) |

| Recognition of foreign judgments | None | Limited | Limited | More receptive to international cooperation |

| Trustee regulator | FSA (Financial Supervisory Commission) | FSRC | IFSC | CIMA |

| English common law base | Yes | Yes | Yes | Yes |

| Adversarial-litigation track record | 40+ years of case law | Solid; less battle-tested than CI | Modeled on CI; lightly tested | Built for institutional finance, not personal AP |

| Typical fit | High-stakes personal asset protection | Moderate exposure; LLC charging-order plays | Cost-sensitive structures | Institutional / fund vehicles |

For head-to-head deep dives, see Cook Islands Trust vs. Nevis Trust and Cook Islands Trust vs. Belize Trust.

How to Establish a Cook Islands Trust

Creating a Cook Islands Trust combines legal drafting, regulatory compliance, and strategic timing. The process follows a clear sequence: define objectives, select a licensed Cook Islands trustee, draft the trust deed (including the duress clause and governing-law provisions), complete AML/KYC due diligence, execute the deed and transfer legal title, establish offshore banking, and begin ongoing administration.

Your trust is typically prepared within 5–7 business days of engagement. The offshore bank account generally takes 30 days or less to establish. Most clients have a fully operational structure within 30 to 40 days.

Fig. 2 — Establishment Timeline

Fully operational in 30 to 40 days.

Consultation

Define objectives. Review exposure. Decide on structure, trustee, and protector.

Drafting

The trust deed is drafted with a duress clause and protector powers.

Trustee & KYC

An FSA-licensed Cook Islands trustee is selected. AML and KYC due diligence is completed.

Funding

The deed is executed. Legal title transfers to the trustee. Offshore banking is established.

Administration

The trustee manages assets on an ongoing basis. The settlor communicates through a structured advisory process.

For a stage-by-stage breakdown, see How Long Does It Take to Set Up a Cook Islands Trust and Choosing a Cook Islands Trustee Company.

Funding the Trust

Once a trust is established, its effectiveness depends almost entirely on how it is funded. Cash and securities move into accounts held in the trustee's name. Operating businesses are typically held through a holding entity placed into the trust. Real estate is held indirectly via an LLC. Cryptocurrency requires secure offshore custody and clear ownership documentation.

The single biggest funding variable is timing. The statute of limitations begins running from the date of transfer, so a trust funded today becomes more defensible with every year that passes without challenge. Transfers made after a legal threat has emerged are significantly more vulnerable.

For the full step-by-step, see Funding a Cook Islands Trust and What Goes in a Cook Islands Trust (and What Doesn't).

Pricing and Timeline

Engagement: $25,000 flat fee. Annual maintenance: $7,000. No hourly billing. The flat fee covers legal drafting of the trust deed, licensed-trustee onboarding, IRS and FinCEN reporting setup, and offshore bank-account establishment. The $7,000/year covers ongoing trustee services, FSA and AML compliance, and continued legal support throughout the relationship.

CPA filings for the required annual reporting (Form 3520, 3520-A, FBAR, Form 8938) typically run $2,000–$3,000 per year and are filed by your CPA, not by Blake Harris Law. Non-standard structures (multiple entities, operating businesses, unusual assets) may be quoted higher, in writing, before any work begins.

For the full pricing breakdown see Cook Islands Trust Cost Breakdown.

Tax Reporting for U.S. Clients

A Cook Islands Trust is tax-neutral. The IRS treats it as a grantor trust, which means all income, gains, and deductions flow through to your personal return as if the trust did not exist. The Cook Islands itself imposes no local income, capital-gains, or estate tax on qualifying structures — but your U.S. obligations remain identical.

Annual filings are required: Form 3520, Form 3520-A, FBAR (FinCEN 114), and Form 8938. Filed correctly, these forms do not increase audit risk.

For grantor-trust treatment in depth see Tax Treatment of a Cook Islands Trust; for the filing mechanics see Reporting Requirements: FBAR, Form 3520, Form 8938.

Confidentiality and Privacy

Cook Islands trusts are not subject to public registration. There is no publicly accessible registry disclosing settlors, beneficiaries, or trust assets. Trustees are bound by strict fiduciary confidentiality obligations, and unauthorized disclosure carries legal consequences. This creates a meaningful layer of privacy — personal and financial information stays out of the public domain and away from casual inquiry.

But this confidentiality is not absolute, and it is important to be precise about its limits. The Cook Islands participates in the Common Reporting Standard (CRS) and the Foreign Account Tax Compliance Act (FATCA). Under these regimes, certain financial information is reported to tax authorities through regulated channels. That information is not available to private creditors, civil litigants, or the public — but it is visible to regulators in specific legal contexts.

The result is controlled confidentiality, not anonymity. And importantly, secrecy is not the main benefit of a Cook Islands Trust. Structures built on legal strength — on the jurisdictional barriers and evidentiary standards of the International Trusts Act — remain effective even when the trust's existence is known. A creditor can know the trust exists. Reaching the assets is still a separate, very difficult undertaking.

What Happens When a Creditor Comes After Your Trust

Understanding how creditors actually pursue Cook Islands Trusts — and why most stop well before reaching the assets — gives a realistic picture of what this structure does in practice.

Fig. 3 — Creditor Pursuit Process

What it costs a creditor to pursue a Cook Islands Trust.

U.S. Judgment

The creditor obtains a money judgment against the settlor in a U.S. court and attempts to enforce it against trust assets.

Not Recognized

U.S. court orders carry no force in the Cook Islands. The creditor cannot enforce the judgment — they must refile entirely.

Files in Cook Islands

The creditor must engage Cook Islands counsel and file a new lawsuit in Rarotonga under Cook Islands law.

Statutory Obstacles

Even a properly filed case faces structural barriers that most creditors cannot overcome:

- —Beyond-a-reasonable-doubt evidentiary standard

- —One-to-two-year statute of limitations on fraudulent transfer claims

- —Cook Islands licensed counsel required — the local bar is small and costly

- —Cash bond typically required to bring suit

- —No fishing-expedition discovery

Settlement

Economics force a resolution. Most cases end here — often before a Cook Islands court is ever engaged.

Step 1: The creditor gets a U.S. judgment. They trace your assets. When they discover assets held in a Cook Islands Trust, they hit a fundamental problem: that judgment has no automatic legal force in the Cook Islands. They cannot register it and collect.

Step 2: Their options narrow. They can attempt to pressure you personally through the U.S. court, seeking orders compelling you to repatriate. But if the trust is properly structured with a duress clause, you no longer have the legal authority to comply — the trustee controls the assets. Alternatively, they can initiate a new case in Cook Islands courts from scratch, hire local counsel, meet the beyond-reasonable-doubt evidentiary standard, and do all of it within the statute of limitations. Most creditors never take that step.

Step 3: Economics force a resolution. Asset protection does not need to make recovery impossible; it needs to make recovery expensive, uncertain, and slow. When a creditor's attorney runs the numbers on Cook Islands litigation against a negotiated settlement, the math almost always favors settlement. Most Cook Islands Trust cases end in settlement, before any Cook Islands court is ever engaged.

When a Cook Islands Trust is challenged, courts focus on three things: intent (was the trust created to defraud a specific creditor?), timing (when were assets transferred relative to the legal threat?), and control (does the trustee exercise genuine independent authority, or does the settlor still run the show?). The last question is usually decisive.

Real Case Law

The cases critics cite to argue Cook Islands Trusts do not work — most commonly FTC v. Affordable Media (the Anderson case) and In re Lawrence — actually demonstrate the structure's strength. In both cases the U.S. court held the settlor personally in contempt for failing to repatriate. But the Cook Islands trustee refused to comply. The assets remained offshore. The structure held.

What failed in those cases was the settlor's ability to demonstrate genuine trustee independence — the court found enough retained practical control to disbelieve the claim of powerlessness. The pattern across every adversarial Cook Islands Trust case is consistent: early establishment, proper funding, genuine trustee independence, and clean documentation produce structures that protect assets. Trusts that cut corners on any of those create personal exposure for the settlor — even when the assets themselves remain offshore and untouched.

For the case-by-case record and the contempt analysis, see Cook Islands Trust Contempt of Court Cases and What If a U.S. Court Orders You to Repatriate Trust Assets?.

The Control Problem

The most common failure in asset protection is not a bad jurisdiction or a poorly drafted trust deed. It is retained control — the natural human instinct to move assets out of reach while quietly maintaining authority over them. Courts understand this instinct, look for it directly, and use it to unravel structures that are otherwise legally sound.

The effectiveness of a Cook Islands Trust turns on a single principle: genuine separation. Not apparent separation, but a real divestment of ownership and decision-making authority. Once assets are transferred, they should not be in the settlor's control in any legally meaningful sense.

A settlor may remain involved in the life of the trust — communicating preferences, articulating investment philosophy, requesting distributions. These are appropriate advisory functions. But that input must leave room for genuine independent judgment by the trustee. If the trustee consistently follows the settlor's wishes without meaningful deliberation, that behavioral pattern becomes the foundation of a control argument in litigation.

The degree of protection a Cook Islands Trust provides is inversely proportional to the degree of control the settlor retains. Settlors who accept this tradeoff — who genuinely defer to trustee judgment — benefit from a structure that has withstood four decades of legal pressure. Those who attempt to preserve both full control and full protection consistently achieve neither.

What Winning Actually Looks Like

One persistent misconception about asset protection is that success means assets perfectly insulated, creditors entirely defeated, and legal threats extinguished without cost or concession. That conception is unrealistic. It also misunderstands how disputes involving protected assets are actually resolved.

In practice, winning rarely takes the form of a definitive courtroom victory. It is far more often reflected in what does not happen.

Opposing counsel, on evaluating the structure, is forced to confront a different set of assumptions: recovery will be jurisdictionally complex, procedurally burdensome, and economically inefficient. In many cases this results in quiet abandonment, narrowed claims, or a decision to pursue more accessible defendants. Where disputes do proceed, success is frequently measured in leverage rather than avoidance. Settlement discussions occur in a different posture when one side faces uncertainty not only about the outcome, but about the enforceability of that outcome.

Asset protection does not eliminate liability; it complicates recovery. And in doing so, it often produces materially better settlement terms. The most effective structures do not produce dramatic courtroom victories. They produce quieter results: cases not filed, claims not pursued, settlements reached on terms that reflect constraint rather than capitulation.

The Single Most Important Variable: Timing

In asset protection, timing is almost always the hidden variable. A trust established years in advance can withstand scrutiny that a trust formed yesterday cannot.

Courts do not evaluate structures in a vacuum. A trust created before a legal problem arises is viewed as legitimate planning. A trust created after a problem appears is viewed through the lens of intent. Why was it done? What was the settlor trying to avoid? These are not drafting questions; they are credibility questions, and credibility is difficult to reconstruct after the fact.

Asset protection is not something that happens during a lawsuit. It is something that should exist before one begins. The best time to establish a Cook Islands Trust is when you do not need it. The second best time is now. For more on the timing question and the fraudulent-transfer clock, see Pre-Litigation Timing and Fraudulent Transfer Concerns.

Deep Dives

The Cook Islands Trust cluster — attorney-reviewed articles grouped by intent. Each one is a self-contained answer to a specific question.

The Cook Islands Trust cluster · 30 articles

How It Works

How the structure works at a legal and operational level.

Trustee, Protector, and Settlor in a Cook Islands Trust

What the settlor, trustee, and protector each do in a Cook Islands Trust — and the structural mistakes that defeat protection.

Cook Islands Trust vs. Offshore LLC — Understanding the Difference

How offshore LLCs and Cook Islands Trusts differ in mechanics, creditor protection, and cost — and why sophisticated plans layer them together.

Cook Islands Trust vs. Domestic Asset Protection Trust

Domestic Asset Protection Trusts vs. Cook Islands Trusts — jurisdiction, creditor protection strength, reporting, cost, and when each fits.

Duress Clauses in Cook Islands Trusts Explained

What a duress clause is, how it works under a U.S. court repatriation order, what it does not do, and why it is central to Cook Islands Trust protection.

Cook Islands Trust vs. Belize Trust — An Honest Comparison

Cook Islands vs. Belize trusts compared — legal framework, statute of limitations, burden of proof, and track record under U.S. creditor attack.

How a Cook Islands Trust Works — A Step-by-Step Guide

A plain-English, step-by-step walkthrough of how a Cook Islands Trust is structured, funded, and operated to protect assets from U.S. creditors.

Cook Islands Trust vs. Nevis Trust — Which Is Stronger?

When people shop for an offshore trust, two names come up more than any others: the Cook Islands and Nevis.

The Cook Islands International Trusts Act 1984 — A Plain-English Guide

A plain-English walkthrough of the Cook Islands International Trusts Act 1984 — the statute behind every Cook Islands Trust, provision by provision.

Setup & Operation

Engagement, funding, reporting, and the timeline from call to funded trust.

Do I Need a Local Attorney for a Cook Islands Trust?

No — proximity is the wrong criterion. What matters for a Cook Islands Trust is counsel whose practice is built around offshore asset protection.

Tax Treatment of a Cook Islands Trust — Grantor Trust Status Explained

Why a Cook Islands Trust is tax-neutral for a U.S. settlor — the grantor trust rules, IRC 679, estate/gift treatment, NIIT, and the common misconceptions.

Cook Islands Trust Reporting: FBAR, Form 3520, Form 8938

The four annual filings a U.S. settlor owes on a Cook Islands Trust — Form 3520, Form 3520-A, FBAR, and Form 8938 — deadlines and penalties.

How Long Does It Take to Set Up a Cook Islands Trust?

Setting up a Cook Islands Trust typically takes four to eight weeks — here is the stage-by-stage timeline, what drives delays, and when a rush is possible.

Funding a Cook Islands Trust — Step by Step

How to move assets into a Cook Islands Trust — which assets can be funded, wire transfer mechanics, IRS reporting, and why timing matters.

What Goes in a Cook Islands Trust (And What Doesn't)

Which assets work well in a Cook Islands Trust, which are complicated, and which are off-limits entirely — a clear-eyed funding inventory.

Cook Islands Trust Cost Breakdown: Setup, Annual Fees

The first question most people ask after learning about Cook Islands Trusts is: what does it cost?

Choosing a Cook Islands Trustee Company — What to Look For

How to evaluate a Cook Islands trustee — licensing, U.S. client experience, financial stability, responsiveness, and the red flags to avoid.

Who It's For

The client profiles a Cook Islands Trust is built for.

Cook Islands Trust for Real Estate Investors

How a Cook Islands Trust layers above property LLCs to protect a real estate investor's liquid wealth from tenant, lender, and GP liability.

Pre-Litigation Timing and Fraudulent Transfer Concerns

How the fraudulent transfer doctrine governs Cook Islands Trust funding — UVTA badges of fraud, Cook Islands vs. U.S. timeframes, and Section 548(e).

Cook Islands Trust for Physicians — Malpractice Asset Protection

Why physicians are exposed to malpractice judgments above insurance limits, and how a Cook Islands Trust protects accumulated personal wealth.

Cook Islands Trust for High-Net-Worth Families

How a Cook Islands Trust serves wealthy families for both creditor protection and multigenerational wealth transfer, alongside estate-tax planning vehicles.

Cook Islands Trust for Cryptocurrency — Protecting Digital Assets

How to hold crypto inside a Cook Islands Trust — custody mechanics, multisig, IRS reporting, and what makes the duress clause work for digital assets.

Cook Islands Trust for Business Owners — Personal Wealth Protection

Why business owners face personal liability that pierces through the LLC veil, and how a Cook Islands Trust protects accumulated personal wealth.

Cook Islands Trust and Divorce Protection — What You Need to Know

What a Cook Islands Trust can and cannot do in a divorce — separate property, community property limits, and the role of a prenup.

Cook Islands Trust: Before vs. After a Lawsuit

A stage-by-stage analysis of Cook Islands Trust timing — what is defensible before, during, and after a lawsuit, and how fraudulent transfer law applies.

Common Questions

The objections, the case law, and the questions worth asking.

What If a U.S. Court Orders You to Repatriate Trust Assets?

What happens when a U.S. court orders a settlor to repatriate Cook Islands Trust assets — the duress clause response and the impossibility defense.

Common Cook Islands Trust Myths — Debunked

Ten common Cook Islands Trust myths — taxes, secrecy, judgment-proof claims, criminal use — and the accurate picture in plain English.

IRS Scrutiny of Cook Islands Trusts — What You Need to Know

What the IRS actually targets in offshore-trust enforcement, why properly disclosed Cook Islands Trusts are not the target, and how to stay compliant.

Cook Islands Trust Contempt of Court Cases — What the Record Shows

What the Anderson, Lawrence, and other Cook Islands Trust contempt cases show about the structure's performance under maximum legal pressure.

Are Cook Islands Trusts Legitimate or a Scam?

The Cook Islands Trust structure is a real legal tool — but the offshore market has bad actors. Here is how to distinguish legitimate engagements from scams.

Are Cook Islands Trusts Legal?

Whether Cook Islands Trusts are legal for U.S. residents — the statutory basis, IRS recognition, court history, and the four conditions that make them lawful.

Working with Blake Harris Law

Blake Harris is an asset-protection attorney focused entirely on offshore structures, with a primary concentration in Cook Islands Trusts. Blake Harris Law is a law firm exclusively focused on offshore asset protection. Blake maintains a global network of licensed trustees, banking relationships, and international advisors, and has co-founded Atlas Trust Company, a licensed Cook Islands trust company.

Every engagement begins with a direct, honest consultation. We assess your risk profile, explain exactly how a Cook Islands Trust would apply to your situation, and give you a clear answer about whether this structure makes sense for you. If it does not, we will tell you that too, and recommend what does.

Frequently asked

Frequently asked questions

Common questions about the Cook Islands Trust — legality, tax treatment, control, cost, and case law — are answered on the dedicated Cook Islands Trust FAQ.